Passenger

Team RideWyze Posted on 13 April 2026

The modern ride-hailing industry is not built merely on maps, cars, or drivers—it is built on in-app payments. What began as a simple mechanism to collect fares has transformed into a complex financial infrastructure involving mobile payments, digital wallets, tokenization, payment gateways, and embedded finance. Every trip today is an invisible financial transaction powered by real-time authorization, risk scoring, and compliance engines.

Ride-hailing platforms realized early that growth would stall without reliable app-based payments. Cash created friction, disputes, and safety concerns, while card-on-file systems unlocked automation and trust. As smartphones became universal, mobile checkout became the gateway to user loyalty. The evolution of these systems mirrors the broader shift from traditional commerce to mobile commerce payments, where the experience is as important as the ride itself.

In the earliest ride-hailing experiments, payments happened outside the application. Riders paid drivers directly, leaving platforms blind to revenue flows. This model limited app monetization, prevented dynamic pricing, and made refunds nearly impossible. Without digital records, platforms could not measure payment success rate or predict earnings.

Cash also restricted innovation. Features like split fares, surge pricing, or subscription passes require automated in-app transactions. The absence of these tools kept ride-hailing closer to traditional taxis than to a scalable tech platform.

Cash introduced social friction: riders worried about carrying the right amount, drivers feared counterfeit notes, and both sides argued about change. The lack of secure in-app purchases undermined trust. Platforms needed a system where money moved silently in the background, creating the foundation for today's digital wallet ecosystems.

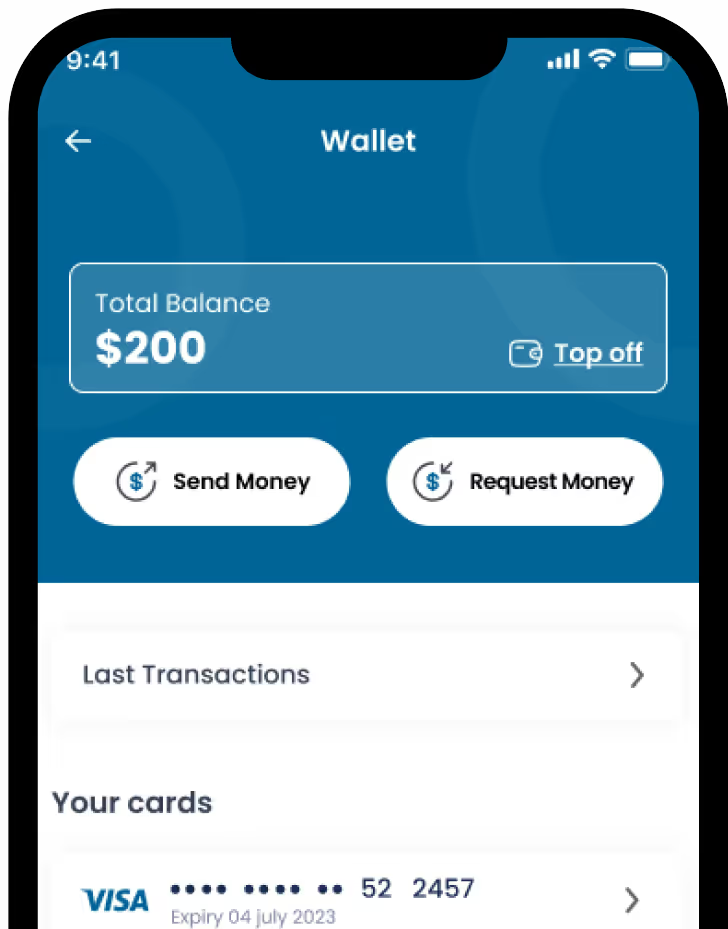

The first breakthrough was storing a payment card inside the app. This simple step birthed true in-app billing. Trips could end with automatic deduction, digital receipts, and transparent pricing. Checkout optimization improved dramatically as riders no longer reached for wallets at the curb.

Card-on-file also enabled ratings and dispute management. Platforms could refund a trip, charge cancellation fees, or credit promotions—all impossible in a cash world. This was the beginning of in-app payments for ride hailing as a strategic asset rather than a utility.

As smartphones matured, global wallets such as Apple Pay and Google Pay joined regional champions like Alipay, GrabPay, and UPI. These wallets delivered one-tap payment and biometric confirmation, reducing drop-offs during mobile checkout. For the first time, payment felt native to mobility, not an external step.

Wallets also opened doors to underbanked users. Prepaid balances, QR funding, and agent top-ups expanded access, proving that mobile wallet integration taxi apps could serve markets where cards were rare.

With scale came risk. Storing raw card numbers inside apps was unacceptable. The industry adopted tokenization in mobile payments, replacing sensitive data with cryptographic tokens. Combined with end-to-end payment data encryption, this aligned ride apps with PCI DSS mobile apps requirements.

Tokenization also simplified recurring billing and refunds. Since tokens are device-specific and useless if stolen, platforms could innovate without exposing users to fraud.

Fraud quickly became sophisticated: account takeovers, promo abuse, and stolen cards. Platforms responded with AI-driven risk engines, 3D Secure mobile, and biometric authentication in-app payments. Behavioral analytics now evaluate every trip—device fingerprint, location history, and velocity checks—before approving a charge.

Security evolved from a compliance checkbox to a competitive differentiator. Riders choose apps where transportation app payment security feels invisible yet reliable.

Building payments from scratch is unrealistic; therefore, ride apps rely on payment SDK integration and mobile payment API for apps offered by gateways such as Stripe, Adyen, and Braintree. These tools manage tokenization, routing, and reconciliation while developers focus on user experience.

Webhooks and orchestration layers allow platforms to switch processors, retry failed charges, and support in-app payment gateway integration across dozens of countries without rewriting code.

Global expansion exposed cultural differences. India demanded UPI integration in ride apps, Brazil preferred PIX payments, and Africa relied on M-Pesa mobile payments. Southeast Asia embraced QR code payments. Successful platforms learned that emerging markets mobile payments require flexibility, not a one-size-fits-all card model.

The pandemic accelerated demand for touch-free interactions. Riders embraced tap-to-pay and NFC integration mobile apps, while drivers displayed QR codes for top-ups and tips. Contactless payments in taxi apps shifted from optional to expected.

Health concerns pushed the idea of "invisible payments." Trips end without any physical exchange; receipts arrive digitally, and gratuities are added with a swipe. This philosophy—payment without interruption—now defines premium mobility.

To stabilize revenue, platforms launched monthly passes and corporate plans using in-app subscription billing and recurring billing. These products increase ARPU mobile and reduce churn by turning occasional riders into members.

Promotions, cashback, and referral credits are powered by in-app purchase optimization engines. Smart incentives lower payment abandonment, nudge users toward preferred methods, and balance supply and demand during peak hours.

Travelers expect their home wallet to work abroad. Modern platforms support cross-border mobile payments, dynamic currency conversion, and localized tax rules. This capability transforms a ride app into a global companion, not a regional service.

For drivers, cashless rides are valuable only if earnings arrive quickly. Platforms now offer A2A transfers, instant debit payouts, and wallet withdrawals, improving retention and trust within two-sided marketplaces.

Many companies provide micro-loans, fuel cards, and insurance, illustrating embedded payments in action. The ride app becomes a financial hub, advancing financial inclusion for gig workers who lacked banking access.

In Asia especially, mobility apps evolved into super app ecosystems offering food delivery, tickets, and bill pay. Payments connect these services through contextual commerce and shared loyalty, proving that transaction infrastructure can redefine an entire digital lifestyle.

Despite progress, obstacles remain: chargeback prevention, KYC/AML obligations, regional data laws, and the complexity of payment orchestration across processors. Balancing compliance such as PSD2 with seamless UX is a constant engineering challenge.

Artificial intelligence will soon choose the optimal method for every trip—credit during promotions, wallet when balance is high, BNPL for long journeys. Such AI-powered payments will lift authorization rates and personalize the checkout completion path.

Experiments with cryptocurrency in-app payments, CBDC mobile wallets, and account-to-account rails hint at a future beyond cards. These models promise lower fees and instant settlement, reshaping mobility economics.

Industry research consistently shows explosive growth: billions of mobile wallet users, trillions in contactless volume, and overwhelming preference for digital over cash. These numbers confirm that in-app payments are not a feature—they are foundational infrastructure for urban transport.

Platforms with superior app payment integration achieve higher approval rates, fewer declines, and stronger network effects. Payments influence pricing, loyalty, safety, and global expansion more than any other module.

The journey from street-side cash to secure in-app payments has redefined how people move through cities. What matters now is not the act of paying but the experience around it—fast, compliant, and almost unseen. As embedded finance apps, voice payments, and wearables mature, the transaction will vanish completely into the ride itself.

In-app payments are no longer the last step of a trip; they are the operating system of modern mobility.

Ride-hailing proved that transportation is a financial product wrapped in a mobility experience. The platforms that master mobile payments, digital wallets, tokenization, and payment gateways will shape the next decade of urban movement—where paying for a ride feels as natural as taking one.

In-app payments improve the ride-hailing experience by removing the need for cash handling and enabling seamless mobile payments directly inside the application. With integrated digital wallets, one-tap payment, and secure payment gateways, riders can complete trips without waiting for change or card machines. These in-app transactions also provide automatic receipts, transparent fare breakdowns, and faster checkout, which increases trust and overall customer satisfaction on ride-hailing platforms.

The payment methods used in ride-hailing in-app payments typically include credit and debit cards, mobile wallets such as Apple Pay, Google Pay, and regional options like UPI, Alipay, and GrabPay. Many platforms also support QR code payments, contactless NFC payments, and stored value wallets to match local preferences. Offering multiple app-based payment options helps companies raise authorization rates and reduce payment abandonment during mobile checkout.

Yes, in-app payments are secure for riders and drivers because modern ride-hailing apps rely on tokenization, PCI DSS compliance, encryption, and biometric authentication such as Face ID or fingerprint login. These security layers protect sensitive card details and prevent fraud in mobile payment processing. Additionally, advanced fraud detection and 3D Secure verification ensure that every in-app transaction is monitored and validated in real time.

Digital wallets and mobile payment gateways help ride-hailing companies grow by enabling fast, reliable, and localized in-app payments for ride hailing across different regions. A strong payment gateway integration improves conversion rates, supports recurring billing like ride passes, and simplifies cross-border transactions. This flexibility allows platforms to expand into emerging markets where mobile wallet adoption and contactless payments are the preferred way to pay.

The future of in-app payments in ride-hailing platforms is moving toward invisible and embedded payments, where transactions happen automatically in the background. Innovations such as AI-powered payment selection, biometric authentication, cryptocurrency options, and super-app ecosystems will make mobile payments even more seamless. These trends will strengthen app monetization and create a fully frictionless mobility economy built around secure in-app billing.

Ready to elevate your ride-hailing business? RideWyze has the tools and expertise to help you succeed. Contact us for a personalized demo today!

Create a free account and get full access to all features for 30 days.No credit card needed. Trusted by over 4,000 Clients.

from 200+ reviews

Start your 30-day free trial.